The Light That Feeds the Machine: Inside the Photonics Supercycle Nobody’s Talking About

Thesis: Photonics is not a thematic trade. It is the mandatory physics upgrade the entire AI industry must execute before the next generation of compute can exist. The companies controlling the critical bottlenecks—CW lasers, epiwafers, and glass substrate processing—sit at the most asymmetric risk/reward inflection point in the semiconductor supply chain today.

Table of Contents

The Market Opportunity

The Core Technology/Mechanism

The Key Bottleneck or Problem

The Players Racing to Solve It

The Economics of the Solution

7 Powers Moat Breakdown

The Fallback Scenario

Risks to the Thesis

Conclusion: Who Owns the Chokepoint?

Introduction

There’s a dirty secret hiding inside every AI press release you’ve read in the last eighteen months. While the world celebrated new parameter counts, multimodal breakthroughs, and reasoning benchmarks, the engineers building these systems were quietly losing sleep over something far more mundane: how do you move data fast enough between chips that the chips themselves don’t become useless?

The answer is light. Specifically, photonics—the technology of generating, manipulating, and detecting photons to transmit information at the speed of light across the nano-distances of a modern data center. And as a cohort of well-researched retail investors have been arguing loudly (if not always coherently) on finance Twitter, the companies enabling this transition are sitting at one of the most compelling structural inflection points in semiconductor history.

This isn’t Quantum Computing. It isn’t a SPAC. It isn’t speculative science fiction waiting for a breakthrough. Photonics is already being deployed at scale by NVIDIA, Google, Microsoft, and Amazon. The question isn’t whether this technology wins. It already has. The question is which of the upstream chokepoints will capture the most economic value from its inevitable scaling, and whether the retail world figures that out before the institutions do.

Spoiler: the institutions are starting to figure it out.

1. The Market Opportunity

Let’s put some numbers around the hype.

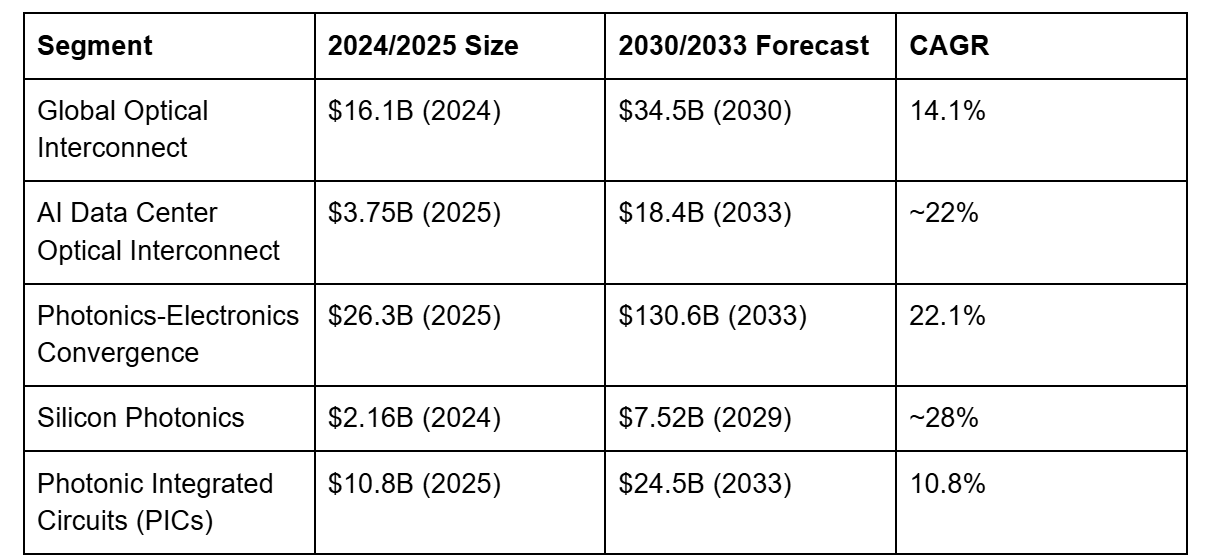

The overall optical interconnect market is undergoing a step-change in trajectory. The global optical interconnect market was estimated at $16.06 billion in 2024 and is projected to reach $34.54 billion by 2030, growing at a CAGR of 14.1%. But that headline figure significantly understates the AI-specific opportunity. The relevant sub-market—optical interconnects inside AI data centers—tells a different story: global optical interconnect in AI data centers reached $3.75 billion in 2025 and is expected to reach $18.36 billion by 2033, implying a roughly 5x expansion in under a decade.

The bigger unlock is the convergence of photonics and electronics at the chip level. The global photonics-electronics convergence technology market reached $26.3 billion in 2025 and is expected to reach $130.6 billion by 2033, growing at a CAGR of 22.1%. That’s not a typo. A five-fold market expansion in eight years, driven by the structural obsolescence of copper-based electrical interconnects in AI hardware.

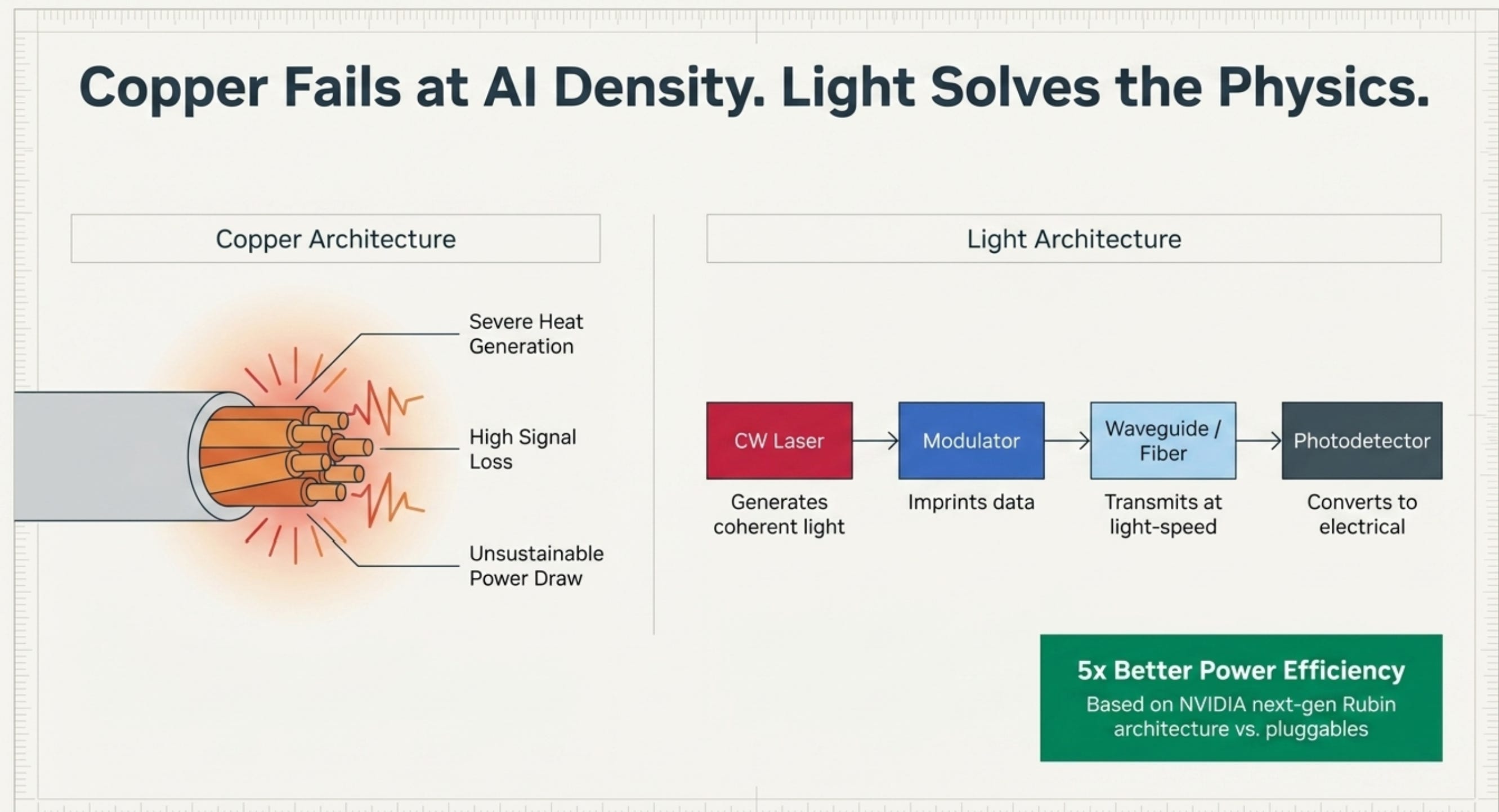

The driving logic is physical, not fashionable. With projections indicating that data centers could consume over 10 percent of the world’s total electricity by 2030, reducing their carbon and energy footprints has become a critical priority. Photonics-electronics convergence addresses this challenge by replacing power-hungry electrical transmission with light. NVIDIA has quantified this directly: its co-packaged optics (CPO) architecture for next-generation Rubin GPUs is expected to deliver five times better power efficiency versus pluggable transceivers.

The growth in addressable market has been catalyzed dramatically by hyperscaler capex. In 2024, Alphabet, Microsoft, Amazon, and Meta invested nearly $200 billion in data center capital expenditures, with this figure expected to climb by over 40% in 2025. This isn’t cyclical spend. It’s structural buildout, and every dollar of that capex creates downstream demand for optical components.

Market Sizing Summary

The claim that photonics TAM goes from $14B to $154B is aggressive but directionally aligned with the higher-end research estimates when you include the broader convergence technology stack—and the numbers keep moving upward every quarter as AI capex surprises to the upside.

2. The Core Technology/Mechanism

To understand why these companies matter, you need to understand the problem they’re solving—and why it’s hard.

Modern AI training clusters require thousands of GPUs working in synchronized parallel. These chips are physically close together (same rack, sometimes same board), but they still need to exchange enormous quantities of data—think terabits per second—with microsecond latency. For decades, this was handled with copper electrical interconnects. Copper is cheap, well-understood, and sufficient up to a certain bandwidth density. Past that point, it simply stops working: too much heat, too much signal loss, too much power draw.

Photonics replaces that copper with light. A continuous wave (CW) laser generates a coherent light source. A modulator imprints data onto that light. An optical fiber or waveguide carries the signal. A photodetector at the other end converts it back to an electrical signal. The whole round trip happens faster and with far less energy than electrons moving through copper.

The key architectural evolution right now is from pluggable transceivers to co-packaged optics (CPO). In a pluggable architecture, optical modules are external to the chip, connected via a cable. CPO integrates the optical engine directly with the switching ASIC or GPU die, dramatically reducing the distance optical signals must travel and improving power efficiency. By integrating photonic interconnects directly with switching ASICs and accelerator silicon, CPO enables ultra-high bandwidth, lower latency, and improved power efficiency. This architecture supports chip-to-chip communication across large AI clusters, making it critical for hyperscale data centers and enterprise HPC environments.

The transition from 800G to 1.6T to (eventually) 3.2T speeds per optical lane is the product cadence driving the current investment cycle. Each generational jump requires higher-power, more precise CW lasers—which is exactly what creates the upstream supply constraint.

The second major technical shift—running parallel to photonics—is the glass substrate revolution in advanced packaging. Organic substrates (ABF, the incumbent) warp at the thermal loads imposed by today’s AI chips. With AI chips now exceeding 1,000 watts of thermal design power and reaching physical dimensions that would cause traditional organic substrates to warp or crack, glass provides the structural integrity and electrical precision necessary to keep Moore’s Law alive. Glass doesn’t warp. Glass has better electrical properties. And forming the through-glass vias (TGVs) that enable multi-die integration on glass requires a very specific, patented laser processing technology.

3. The Key Bottleneck or Problem

Here is where the investment thesis crystallizes.

Photonics has won the architectural competition. The question is no longer if hyperscalers adopt optical interconnects at scale—it’s how fast they can ramp. And ramping is brutally hard because the supply chain for photonic components is extraordinarily thin.

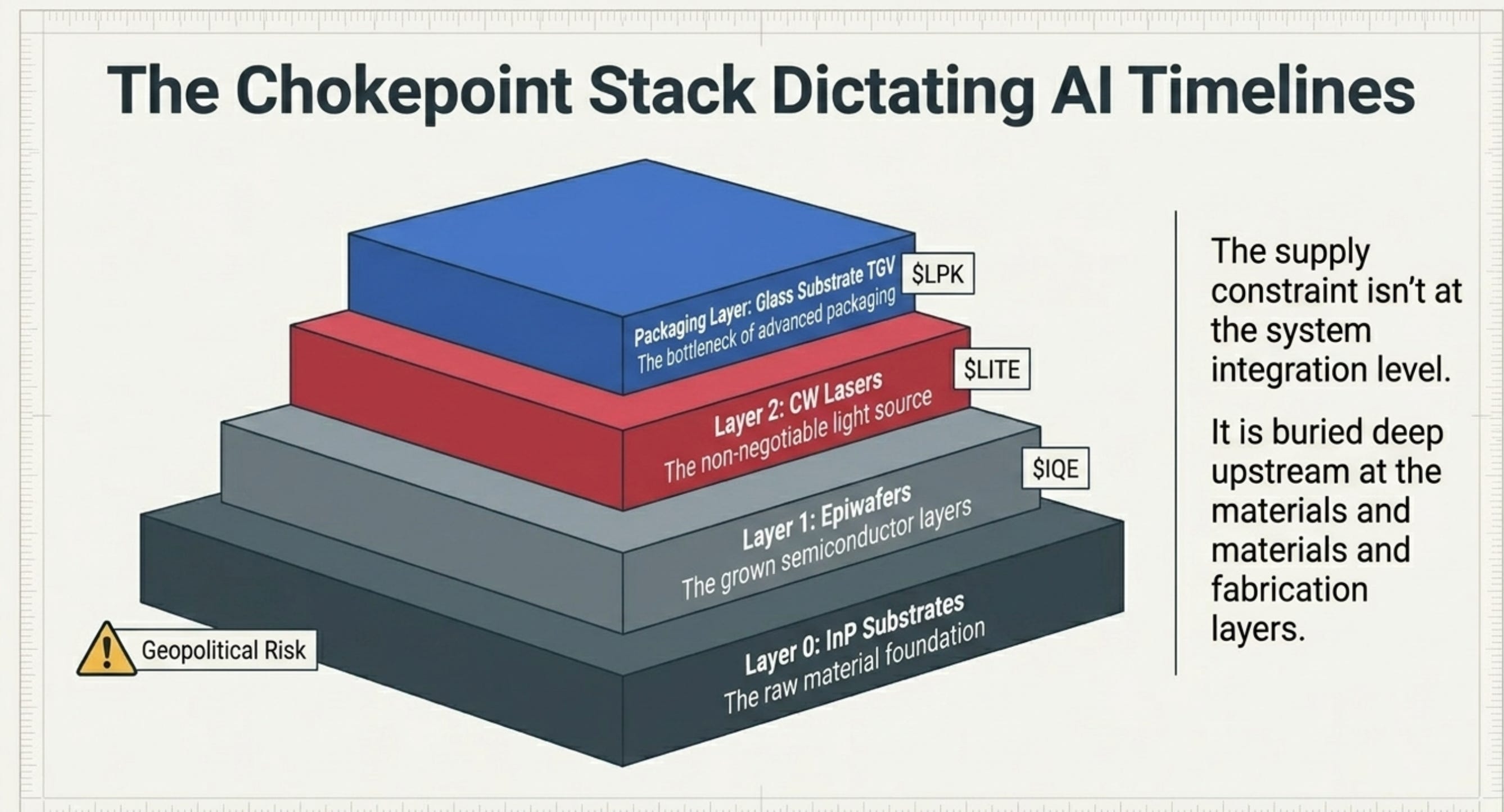

The supply constraint isn’t at the system integration level. It isn’t at the transceiver module level. It is deep upstream, at the materials and fabrication layers that almost nobody in the investment community tracks.

Layer 0 — InP Substrates: Indium Phosphide (InP) is the substrate material of choice for high-performance lasers. It’s harder to manufacture than GaAs. One challenge for 6-inch InP pertains to substrate supply, more specifically the cost. The current price for 6-inch InP is a challenge. Certainly, the price will come down as volumes increase, but InP substrate manufacture is more challenging than GaAs, so yield is likely to be a factor, particularly at the larger wafer diameter. China added InP to its export control list in February 2025, adding geopolitical fragility to an already constrained supply chain.

Layer 1 — Epiwafers: On top of the InP substrate, compound semiconductor layers are grown via epitaxial deposition. This is IQE’s domain. IQE sits as a monopoly-scale epiwafer supplier invisible to US capital. MACOM MTSI is quietly qualifying CW lasers that feed the entire SiPh ecosystem. When CPO deployments ramp, the volume demand for epiwafers becomes the production bottleneck, not just a strategic consideration.

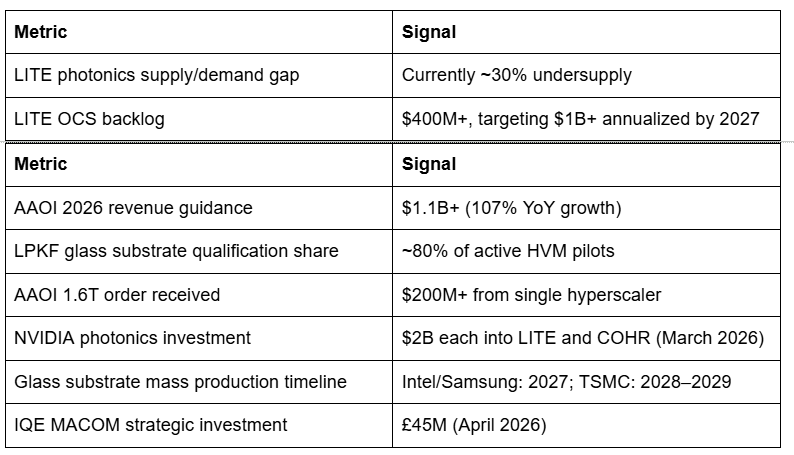

Layer 2 — CW Lasers: The continuous wave laser is the light source for co-packaged optics. You cannot build CPO without it. Lumentum disclosed in its Q2 2026 earnings call that photonics demand is currently outstripping supply by about 30%. This is a 30% structural shortage in the most critical component for AI optical infrastructure. The immediate implications of this backlog are profound, signaling that the bottleneck in AI development has shifted from raw compute power to the optical “connective tissue” that links tens of thousands of GPUs together.

Glass Substrate Layer — TGV Processing: In the advanced packaging domain, the bottleneck is via formation in glass. LPKF invented LIDE (introducing it around 2017) and heavily patented it. While competitors are researching alternative plasma or laser solutions, LIDE is currently the only commercially viable, HVM-ready solution that preserves the structural integrity of the glass.

The supply chain, in short, is a stack of chokepoints all the way down. And none of them resolves quickly—fab construction takes years, and qualification processes with hyperscaler customers add another 12–24 months on top of that.

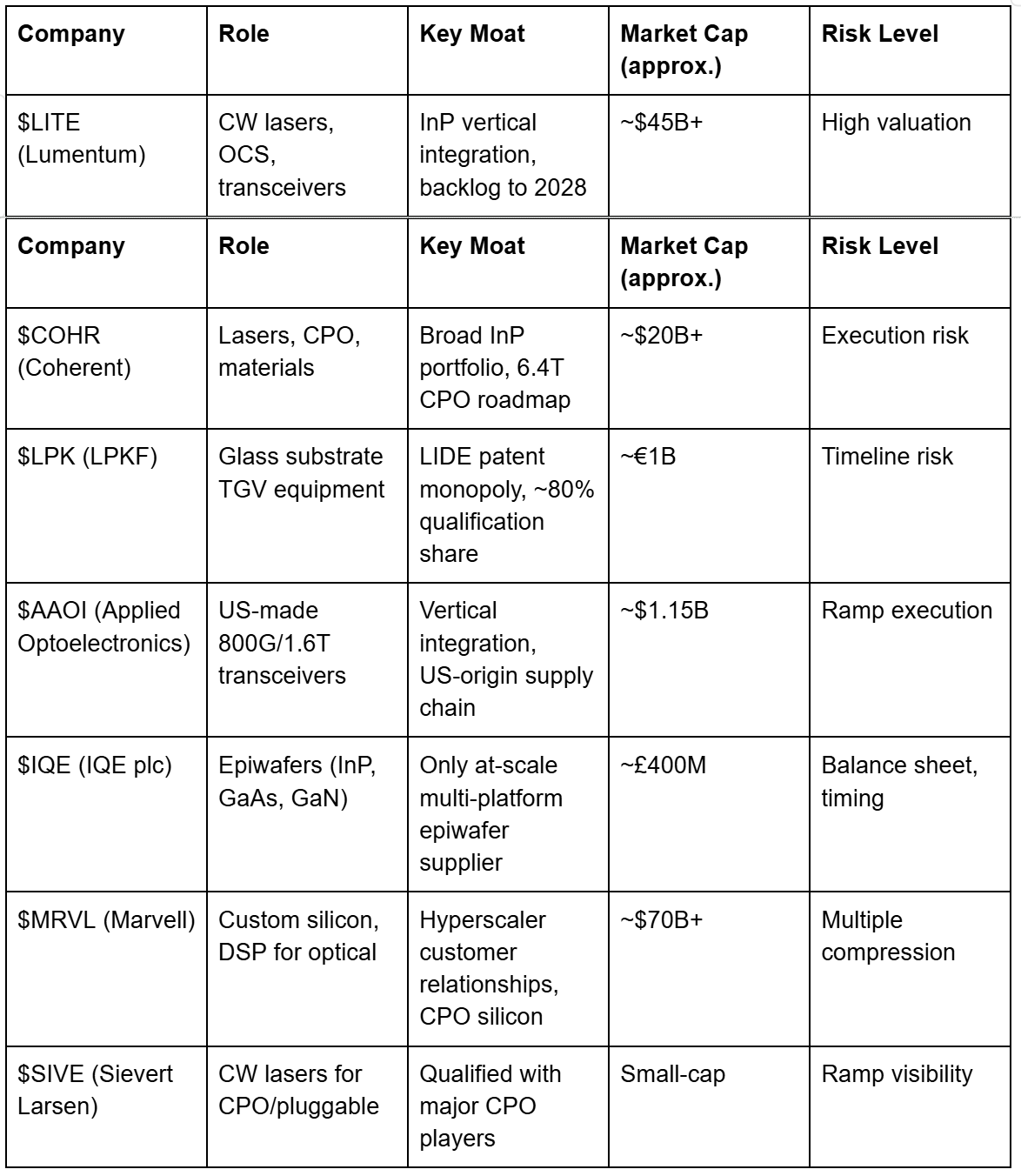

4. The Players Racing to Solve It

Four specific companies as asymmetric plays on the photonics supercycle. Let’s examine each with fresh data:

$LITE — Lumentum Holdings: The Incumbent Throne

Lumentum is the photonics bellwether. Its valuation has reflected this: LITE has delivered a staggering ~989% return over the past 12 months, surging from the $70–$80 range in early 2025 to over $800 per share by March 2026. The template—a company that went “from $2B to $80B”—and the arc of that story is precisely the roadmap the smaller players are trying to replicate.

What drove the re-rating? Lumentum Holdings reported that its manufacturing capacity for critical AI components is effectively sold out through the end of 2028. A company that is literally unable to sell more product because it can’t make it fast enough—that is a supply-constrained monopoly, and markets reward those violently when they’re discovered.

The NVIDIA relationship is particularly telling. In late March, the company announced plans to establish a new manufacturing facility in North Carolina to produce advanced indium phosphide-based optical devices such as continuous wave and ultra-high-power lasers for AI data centres. However, the new site is not expected to begin volume production until mid-2028. Even with emergency capacity expansion, the supply shortage extends 2+ years. Management’s $2 billion quarterly revenue target by 2028—implying approximately $8 billion in annual revenues—is now viewed by analysts as credible rather than aspirational.

$LPK — LPKF Laser & Electronics: The Glass Gateway

The claim of “~80% market share in qualifications” aligns with industry consensus. Nearly every major player standing up pilot lines for glass—Intel, Absolics, Samsung, LG Innotek, Corning—is either actively testing, licensing, or directly buying LPKF’s equipment to process their glass.

LPKF’s LIDE technology is not just dominant—it appears to be the only HVM-ready solution. The glass substrate transition is accelerating: the first commercial products to feature full glass core integration are expected to hit the market in late 2026 and early 2027, likely appearing in NVIDIA’s “Rubin” architecture and AMD’s MI400 series accelerators.

The emerging CPO-on-glass angle is even more interesting. LPKF is also conducting research on the topic of CPO on glass substrates. “We are already working, since more than 2 years, with a semiconductor partner from the US in exclusive development on the topic of co-packaged optics”—with strong circumstantial evidence pointing to Intel as that partner. This positions LPKF at the intersection of both supercycles: advanced packaging and photonic integration.

$AAOI — Applied Optoelectronics: The American Challenger

AAOI is the most operationally complicated story in this cohort—it’s also potentially the most compelling for investors with a risk appetite. While the Chinese optical transceiver industry (Innolight, Eoptolink) dominates current production, AAOI is building what the source describes as “the largest Made in America supply chains for both CW laser fab, as well as 800G, 1.6T assembly.”

The numbers are starting to show up: “We completed our first volume shipment of our 800G products to one of our large hyperscale customers in Q1. Looking ahead, we continue to anticipate a strong volume ramp of our 800G products starting in Q2 and we anticipate sequential revenue growth throughout this year, with significantly larger growth expected starting in Q3 as additional capacity comes online.”

AAOI has received more than $124 million in 800G orders from one major hyperscale customer and a 1.6T transceiver order worth more than $200 million from a long-term hyperscale customer. Management has raised full-year 2026 guidance to over $1.1 billion—a 107% year-over-year increase if achieved. The diversified supply chain—making the entire stack in-house—gives AAOI unique optionality across technology generations that pure-play component suppliers don’t have.

The risk: the company expects to expand manufacturing operations in the U.S. and Taiwan during 2026 and 2027 primarily to support laser diode production and production of 800G and 1.6T transceivers. Execution on that ramp is the make-or-break variable.

$IQE — IQE plc: The Invisible Floor

IQE is the compound semiconductor epiwafer supplier that the entire Western optical supply chain depends on—and which barely registers in mainstream investment coverage. MACOM is investing £45m, including £30m in equity plus £15m in new secured zero-coupon convertible loan notes. On completion of its investment, MACOM will enter into long-term strategic supply agreements with IQE, enabling scalable, high-volume manufacturing across key growth segments.

This is precisely as described—MACOM (MTSI) paying off IQE’s debt because they can’t afford to have their upstream epiwafer supplier go under. IQE is the only supplier with the scale and expertise across all major epitaxy platforms (MOCVD and MBE) combined with the industry’s broadest portfolio of materials, including GaAs, InP, GaSb and GaN.

The investment case is less about near-term revenue and more about optionality and floor: the moment CPO volume ramps materially, IQE’s epiwafer capacity becomes the binding constraint on the entire optical supply chain. You don’t want to be the company that needs 10x more epiwafers and has no idea where to get them.

Competitive Landscape Summary

5. The Economics of the Solution

Here is where the broader strategic argument lives: it’s not enough to supply lasers. The economic prize goes to the companies that expand vertically through the stack.

The logic is intuitive once you see it. A raw CW laser chip might sell for $50–$200. The External Laser Source (ELS) module built around that laser sells for significantly more. The entire CPO optical engine sells for more still. And if you can integrate that engine into a complete pluggable transceiver or co-packaged module, you’re now capturing gross margin at every layer you pass through.

This is exactly what Lumentum did with its acquisition of Cloud Light (transceiver assembly), and what Coherent has done by integrating up the stack from InP wafer fabrication into finished modules. The most transformative move came in late 2023 with the acquisition of Cloud Light, which allowed Lumentum to move “up the stack” and design fully assembled optical transceivers, setting the stage for its current dominance in the AI infrastructure market.

The gross margin mathematics of vertical integration are compelling:

Raw epiwafers: 30–40% gross margins

Laser chips: 40–55% gross margins

Complete transceivers: 45–65% gross margins (at scale)

Optical Circuit Switches: potentially 60–70%+ gross margins (differentiated, limited competition)

For AAOI specifically, the path to margin improvement runs through 800G and 1.6T mix shift. Management raised full-year 2026 revenue guidance to over $1.1 billion, and expects non-GAAP operating income to exceed $140 million, driven by robust demand for 800G and 1.6T transceivers. Non-GAAP operating margins approaching 13%+ on a revenue base that wasn’t $200M three years ago represents a genuine business transformation.

For LPKF, the math is different but equally attractive. The glass substrate equipment market is, at its core, a capex leverage play: as Intel, Samsung, and TSMC collectively spend billions qualifying glass substrate lines, each unit of that capex routes disproportionately through LPKF’s LIDE systems. LPKF is perfectly positioned as the ultimate “picks and shovels” play for the glass era. Equipment suppliers capture revenue upfront and then enjoy a recurring aftermarket in spare parts and service—structurally high-margin businesses.

6. The 7 Powers Moat Breakdown

Hamilton Helmer’s 7 Powers framework maps competitive advantage to sustainable economic surplus. Here’s how it applies to each key player:

Verdict: Lumentum and LPKF have the deepest moats by the 7 Powers framework. IQE’s cornered resource position is structurally compelling but financially fragile. AAOI’s counter-positioning on US-origin supply is real but not yet durable—they’re building moat, not defending it.

7. The Fallback Scenario

No bull case is complete without a sober look at what happens if it doesn’t work.

If the photonics transition stalls—due to CPO yield issues, technology substitution, or simply hyperscaler capex retrenching—the fallback scenario differs significantly by company:

Lumentum: Even in a slowdown, LITE retains its 2028 backlog and the OCS business, which is largely incremental to pluggable revenue. The floor is a return to telecom-paced growth (~10% annually) with a much higher earnings base than 2023. The risk is multiple compression from AI-premium pricing—a stock at 85x forward earnings doesn’t survive a growth deceleration gracefully.

LPKF: If glass substrate timelines slip further (this has happened before—semi packaging timelines are notoriously optimistic), LPKF faces a significant revenue air pocket. The company’s base business in PCB laser systems provides some cushion but not enough to justify current valuations predicated on glass volume arriving 2027–2028. Semi timelines are notoriously slow. “Imminent” mass production for advanced packaging means a slow ramp-up peaking between 2026 and 2028.

AAOI: The most operationally leveraged and the most fragile in a slowdown. High capex, still-improving gross margins, and a revenue base that’s growing fast but not yet throwing off significant free cash flow. A hyperscaler pause would hit AAOI disproportionately.

IQE: Paradoxically, IQE’s precarious financials mean the fallback scenario is essentially “keeps surviving at low valuation.” The MACOM strategic investment has stabilized the balance sheet. On completion of its investment, MACOM will enter into long-term strategic supply agreements with IQE, enabling scalable, high-volume manufacturing across key growth segments. The risk isn’t irrelevance—it’s timing. If the InP volume wave takes three more years to arrive, IQE can survive but won’t thrill shareholders.

8. Risks to the Thesis

The photonics bull case is compelling. These are the genuine threats:

1. Silicon Photonics Disruption The most credible technology risk is Silicon Photonics (SiPh) eventually displacing InP-based components. By 2028, roughly 44% of optical transceivers are expected to use silicon photonics, up from 24% in 2022. Silicon is abundant, integrates with standard CMOS processes, and costs less to manufacture at scale. The limitation today is that silicon can’t generate its own light efficiently—you still need an InP laser as an external source. If this changes (GaN-on-silicon lasers, for example), the InP moat erodes significantly.

2. Geopolitical Supply Chain Risk InP substrates are on China’s export control list. A significant portion of raw indium comes from Chinese mining operations. An escalating tech war that restricts indium or InP exports would create acute supply disruptions across the entire photonics stack—potentially including LITE, COHR, and IQE simultaneously.

3. Hyperscaler Capex Retrenching The current photonics boom is predicated on continued massive data center investment. In 2024, Alphabet, Microsoft, Amazon, and Meta invested nearly $200 billion in data center capital expenditures, with this figure expected to climb by over 40% in 2025. Any meaningful pullback in that spend—driven by AI ROI concerns, credit conditions, or macro deterioration—would cascade upstream quickly.

4. CPO Yield and Integration Timelines Co-packaged optics is technically difficult. Integrating photonics with advanced silicon at the package level requires solving thermal, alignment, and yield challenges that are not fully resolved. If CPO deployment timelines slip 2–3 years, the CW laser demand wave that underpins LITE and IQE is deferred, not cancelled.

5. Competition for LPKF Heavyweight equipment manufacturers like Applied Materials and laser giants like Coherent are absolutely pouring R&D into engineering their own TGV solutions. LPKF’s LIDE patent position is strong but not impenetrable. Applied Materials in particular has the scale and R&D budget to develop competitive alternatives, and Intel’s own 600+ glass substrate patents represent a potential licensing leverage point.

6. Valuation Risk at the Top LITE has already done its 10x. Investors buying today are paying for the next 10x, which requires everything to go right: capacity expansion, OCS ramping to $1B+ annually, margins expanding, and CPO adoption accelerating. At 85x+ forward earnings, there is essentially no margin of safety. At all-time highs, every negative datapoint—a hyperscaler guidance cut, a margin miss, a competitive qualification loss—will be magnified by a stock with no margin of safety priced into it.

9. Conclusion: Who Owns the Chokepoint?

The photonics supercycle is real. The physics is settled. The architecture is decided. The money is flowing. What remains uncertain—and where the investment opportunity lives—is which players capture the value, and on what timeline.

The hierarchy of chokepoints, ranked by current defensibility:

EML/CW Laser Fab Capacity (LITE, COHR): The most immediate and most priced bottleneck. Demand exceeds supply by ~30%. Lumentum’s backlog is booked to 2028. NVIDIA has written $2B checks to both Lumentum and Coherent simultaneously to guarantee supply. When your customer is so desperate for your product that they’re providing strategic financing, you own a chokepoint.

TGV Glass Substrate Processing (LPK/LPKF): The highest-quality asymmetric opportunity in this set. ~80% qualification share, unique technology, a market that hasn’t fully turned on yet. The risk is timing; the reward is significant if glass substrate adoption hits the 2027–2028 mass production window that Intel, Samsung, and TSMC are all targeting.

Epiwafer Supply (IQE): The deepest and most underappreciated chokepoint. MACOM’s £45M strategic investment—structured as a lifeline and a supply lockup simultaneously—tells you everything you need to know about how the smart money views IQE’s strategic position. The financial fragility is real; so is the strategic indispensability.

US-Origin Transceiver Assembly (AAOI): The highest-execution-risk play, with the largest upside if the revenue ramp delivers. The US supply chain narrative is real (tariffs, reshoring, sovereign AI infrastructure), the orders are real ($324M+ backlog), and the $1.1B 2026 revenue guidance is achievable. This is a “show me” story at this stage—but what it’s showing is increasingly impressive.

What to Watch

LITE backlog commentary in quarterly earnings (any signs of order pushouts?)

LPKF equipment orders from Intel, Samsung SEMCO, and LG Innotek (the H2 2026 / H1 2027 ordering cycle)

IQE capacity announcements and any additional strategic partnerships beyond MACOM

AAOI 800G shipment volumes beginning Q2 2026 and 1.6T ramp in Q3

CPO deployment milestones from NVIDIA (Rubin architecture, expected 2027 sampling)

InP export control developments from China

Key Data Points

The core argument deserves to be taken seriously: this isn’t a trade, it’s an architecture. Photonics is to the AI era what TSMC’s leading-edge nodes were to the smartphone era—mandatory infrastructure that scales for a decade, rewards early moat-holders disproportionately, and gets discovered slowly by retail capital while institutions accumulate quietly.

The question isn’t whether light wins. Light already won.

The question is whether you got there before the institutions—or after.

“The next generation of AI runs on light. The companies that make the light, grow the crystals that make the light, and drill the holes that package the light are sitting at the most asymmetric supply chain in semiconductors today.”

Disclaimer: This is not financial or investment advice. Nothing in this piece constitutes a recommendation to buy or sell any security. All analysis is based on publicly available information and is provided for educational and entertainment purposes only. Markets are forward-looking and inherently uncertain. Do your own research. Speak with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results. The author may hold positions in securities mentioned.